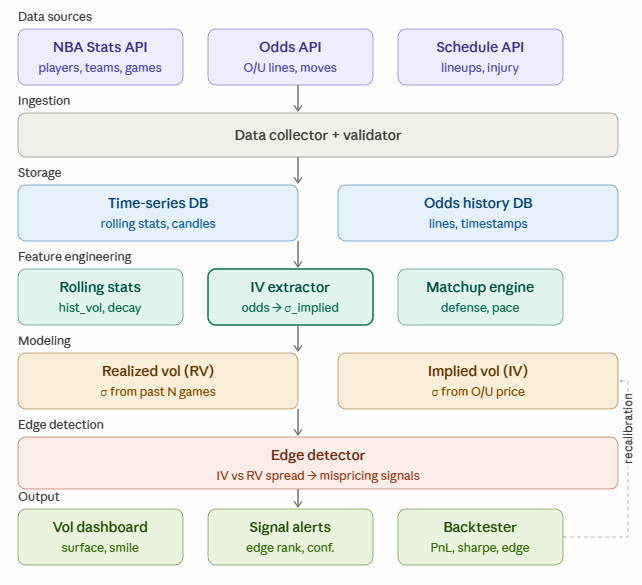

Continuing my quantitative analysis system that applies the concepts of implied volatility in options markets to the NBA, by extracting a player sigma directly from the Over/Under lines of bookmakers to detect statistical mispricing.

Here is the end-to-end data pipeline collecting player stats (NBA API), O/U odds (Odds API) and matchup data, to calculate realized volatility (rolling STD of performances) and implied volatility (reversal of bookmaker pricing) in parallel, then identify exploitable IV/RV spreads.

Inspired by the analysis of aurelius.v.1, I also integrated an analysis of the feeling opposing fans and the media.

Being an observer of this sport since the 2010s, the criteria that made a player good or that a team was good at the time are no longer the same as today.

I am thinking in particular of V. Wembanyama who is a revolution at his post.

We can also ask ourselves questions about the impact of social networks then and now. For example, one might ask whether Mr. Jordan would have been even more popular today than 30 years ago? What impact would his communication have had today on the feeling of the public and the media?

The next step for me in this project will be to find an advantage.

A system that extracts the implied volatility from the O/U NBA lines to detect discrepancies with players' historical realized volatility, amplified by a social sentiment analysis that anticipates mispricings before they form in the line.

I look forward to your observations and comments!

Good day everyone!

Dans la continuité de mon système d'analyse quantitative qui applique les concepts de volatilité implicite des marchés d'options à la NBA, en extrayant un sigma joueur directement depuis les lignes Over/Under des bookmakers pour détecter les mispricings statistiques.

Voici la pipeline de données end-to-end collectant stats joueurs (NBA API), cotes O/U (Odds API) et données de matchup, pour calculer en parallèle une volatilité réalisée (rolling std des performances) et une volatilité implicite (inversion du pricing bookmaker), puis identifier les spreads IV/RV exploitables.

En m'inspirant de l'analyse de aurelius.v.1, intégré également une analyse de sentiment opposant fans et médias.

Etant observateur de se sport depuis les 2010, les critères qui faisaient qu'un joueur était bon ou qu'une équipe était bonne à l'époque ne sont plus les mêmes qu'aujourd'hui.

Je pense notamment à V. Wembanyama qui est une révolution à son poste.

On peut également se questionné sur l'impacte des réseaux sociaux à l'époque et aujourd'hui. On peut par exemple se demander si M. Jordan aurait été encore plus populaire aujourd'hui qu'il y a 30 ans ? Quel impacte aurait eu sa communication aujourd'hui sur le sentiment du public et des médias ?

La suite pour moi de se projet sera de trouver un avantage.

Un système qui extrait la volatilité implicite des lignes O/U NBA pour détecter les divergences avec la volatilité réalisée historique des joueurs, amplifié par une analyse de sentiment social qui anticipe les mispricings avant qu'ils se forment dans la ligne.

J'attends vos observations et vos commentaires !

Bonne journée à tous !

Thank you for sharing! Eager to see more in the context of your backtests, covariance structures, and so on, there are a lot of sources of data and methods to construct sharp odds to quote prices too, curious of implications here in optimizing market making too