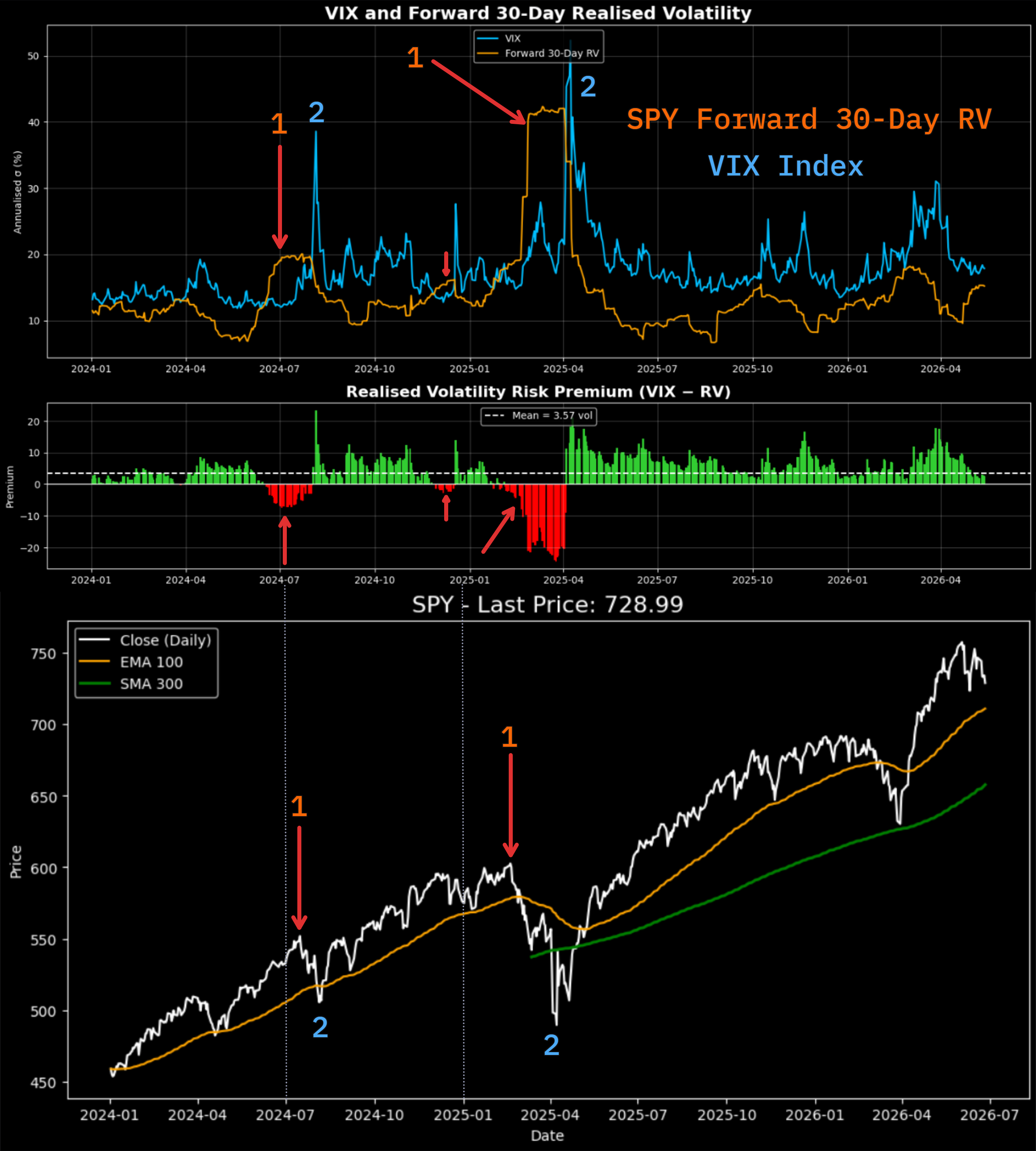

The key insight is simple: implied volatility, what the options market thinks will happen, almost always overestimates what actually happens. The VIX Index, which represents the market’s 30-day volatility forecast for the S&P 500, has overestimated realized volatility roughly 80% of the time over the past two decades.

That gap between what the market expects and what actually unfolds is called the Volatility Risk Premium (VRP).

Why does this premium exist? Because volatility tends to spike when equities fall. Portfolio managers buy protection through options and variance swaps, and the pool of risk-averse buyers persistently exceeds the pool of sellers willing to warehouse that risk.

If eVRP is positive, the market is pricing in more volatility than recent history suggests. The premium looks attractive. If eVRP is negative or zero, the market might be underpricing risk